Constitutional and statutory requirements for governments to balance their budgets are increasingly standard, especially as part of a plan to reduce fiscal stress. They help policymakers keep spending and revenue trends closer together, so the debt burden falls as debt grows slower than the economy.

Even a longtime skeptic of deficit reduction like President Biden’s chief economist Jared Bernstein recently wrote that “I, like many other longtime doves, am joining the hawks, because our nation’s budget math just got a lot more dangerous.”1

Limiting borrowing reduces debt’s drag on opportunity and prosperity. It also encourages questions—and good answers now exist—about managing the budget holistically and with contributions from many legislators to make achieving and sustaining balance possible.2

Amending the U.S. Constitution requires an exceptional degree of consensus: usually, two-thirds of both houses of Congress and three-fourths of state legislatures.

Despite its flaws, one balanced budget amendment (BBA) came close to approval in 1995. Today, better BBAs exist. 3

Better policy, good politics, and an inclusive process4 could be the key to adopting a reasonable constitutional fiscal rule and statutory upgrades to strengthen fiscal democracy in America.

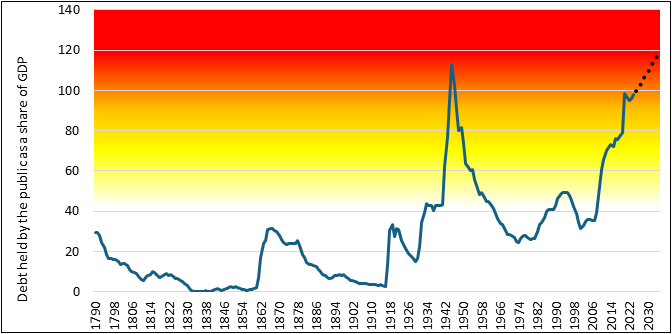

Figure 1. High & rising debt undermines prosperity, threatens crisis

Source: CBO’s January 2025 Budget and Economic Outlook

The debt burden – the ratio of debt held by the public to gross domestic product – is on track to rise indefinitely. Excessive debt undermines prosperity by absorbing funds that could have been used for productive investments and by increasing uncertainty about future government spending and revenue policies. A high debt burden can also increase interest rates paid by governments and consumers while creating inflationary pressure.

The level of public debt where this damage begins is contested. Estimates range from 43 percent to 114 percent with a mean and median of 74 and 76 percent, respectively.5 The U.S. federal government’s debt-to-GDP ratio is about 100 percent today. Debt damage grows as the debt burden increases, perhaps at an exponential rate.

As debt surges, so does the risk of fiscal collapse. A debt crisis could devastate American prosperity, opportunity, security, and even our way of life.

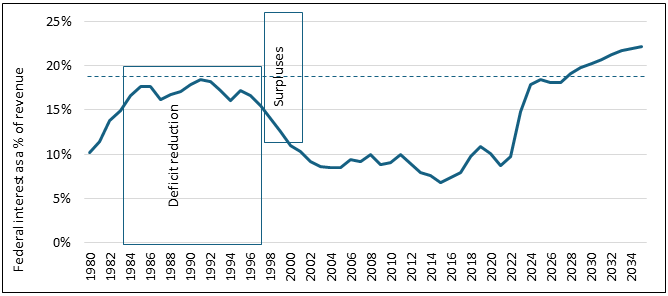

Figure 2. Federal interest expense is high compared to revenue

Note: Includes OBBBA effects

Source: CBO, author’s calculations

The debt-service-to-income ratio is a standard measure of financial resilience in the private sector. The federal government’s chronic deficits and surging inflation in the 1970s and early 1980s produced a near-doubling of federal interest expenses as a share of federal revenue in the 1980s.

Members of Congress of both parties and Presidents Reagan, Bush, and Clinton enacted a series of deficit-reducing bills. After nearly fifteen years, the federal government’s unified budget was in surplus, albeit with help from the end of the Cold War, a long period of economic growth, the tech boom and associated elevated revenue, and the large Baby Boom generation in its peak-earning years, which led to Social Security surpluses as well.

The COVID-19 pandemic coincided with the end of the global savings glut, which had pushed down global interest rates for a generation. In addition, surges in federal borrowing around the Financial Crisis of 2008 and the COVID-19 pandemic, the retirement of the Baby Boom generation, major overseas military continencies, and other factors have increased the debt burden from 35 percent of GDP in 2007 to 100 percent today.

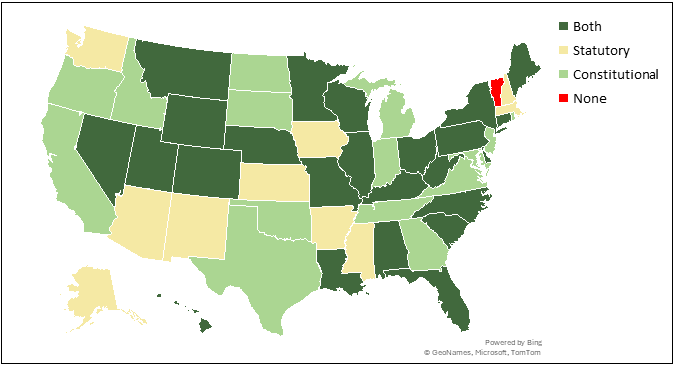

Figure 3. U.S. states have constitutional and statutory balance rules*

*Balance requirements apply at one or more stages of the budget process

Source: National Association of State Budget Officers6

Nearly every state has a combination of constitutional and statutory rules requiring them to balance their budgets. The rules typically exclude capital investments such as transportation assets and buildings from near-term balance, but those facilities are expected to generate value commensurate with borrowing costs over their useful lives.

States did not spring into being with rules for fiscal responsibility. Extensive borrowing in the early republic – often for canal-building in the north and capitalizing small banks in the south – led states into financial distress in the early 1840s. Bond buyers demanded structural changes to state policies including debt limits and balanced budget rules. These carried over into newly formed states and expanded again after state and municipal financial troubles in the 1870s and 1930s.

In addition to formal rules, bond markets support responsible budgeting in the states. Bond markets impose risk premiums on state bonds that reflect underlying risks, and state policymakers often take pride in low financing costs. And, of course, the states cannot print money to supplement taxation and borrowing.

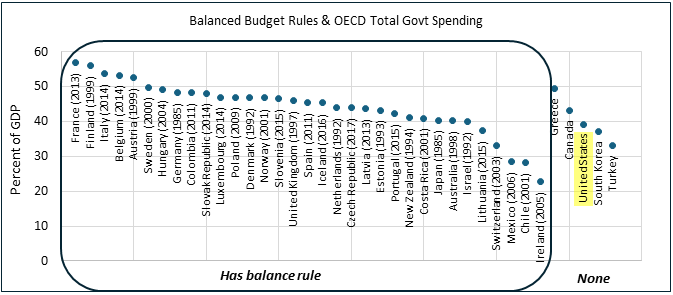

Figure 4. Most high-income countries balance, but at diverse spending levels

Source: IMF7

Adopted balanced budget rules do not specify the size and scope of government. Political culture and other institutional factors determine a country’s level of taxpayer-supported public services and their allocation between national and sub-national governments.

Thirty years ago, balance rules were rare among prosperous countries. Today, they are ubiquitous. The size of government and current debt burdens vary, but balance rules help countries slow and reverse their debt growth. The United States is now an outlier.

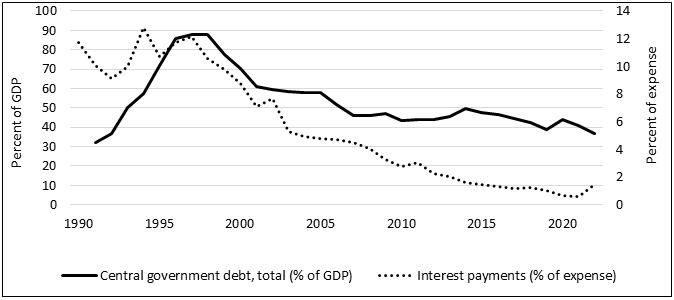

Figure 5. Controlling debt reduced Sweden’s interest expense

Source: World Bank

Low economic growth and a surge in spending – causality runs both ways – drove Sweden’s debt burden from 30 to nearly 90 percent of GDP in the 1990s. Interest payments consumed as much as 12 percent of spending, and even more as a share of revenue.

This fiscal stress drove policymakers to adopt a series of policy and institutional changes. They did not do everything at once. They did as much as they could agree on within the bounds of the politically possible over a thirty-year period. They persisted in streamlining policies, largely by improving spending efficiency, and by upgrading their institutional architecture to expand the possibilities for further changes.8

Reduced interest expense reflects not only a declining debt burden but also lower interest rates as global bond buyers recognized the improving trajectory of fiscal sustainability.

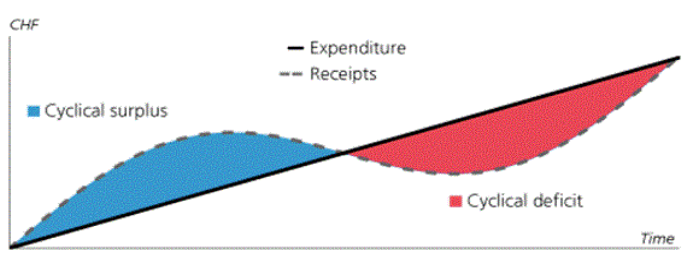

Figure 6. The Swiss debt brake’s “structural balance” is a model of success

Source: Swiss Confederation

Switzerland also experienced fiscal stress in the 1990s, but at a much lower debt burden. Swiss government is highly decentralized with much policy made in the cantons (subnational government akin to U.S. states), and increasing national taxes requires a vote of the people in a referendum.

After years of deliberation about designing a balance rule, the national legislature referred a constitutional amendment to the voters, who approved it 84.7 percent in December 2001. It became effective in 2003, and the legislature enacted implementing legislation in October 2005 to clarify terms and processes.9

The Swiss debt brake limits spending to cyclically-adjusted revenue: the revenue the government would collect if the economy grew perfectly on trend. During booms, revenue exceeding this spending limit (blue area) reduces outstanding debt or is placed into a reserve fund. During recessions and emergencies, the government can draw on reserves or borrow (red area) in global markets at low rates.

This “structural balance” approach ensures that the budget balances over the medium term while allowing actual deficits and surpluses to vary with the business cycle. It gives policymakers a stable and predictable platform for budgeting.

The Swiss debt brake also requires offsets to emergency spending, but offsets are subsequent, not concurrent with urgent needs. The payback period depends on the size of the outlay, generally three or six years, but it can be extended in extraordinary circumstances.

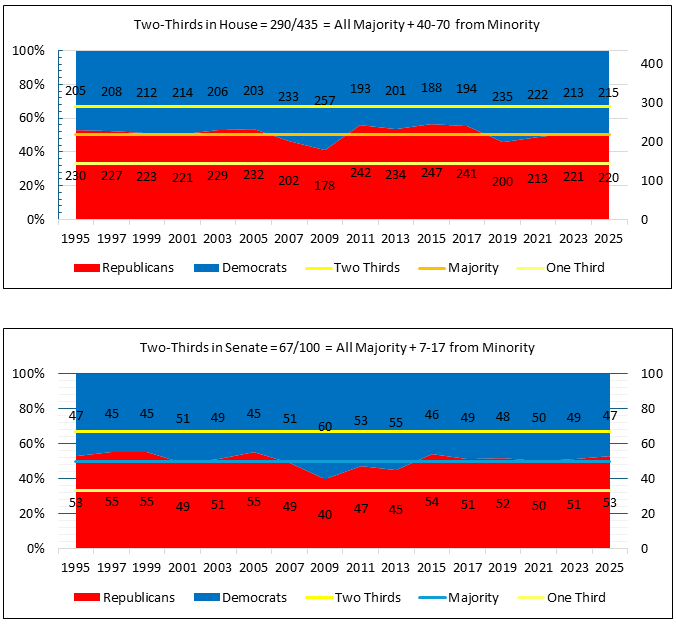

Figure 7. Two-thirds of Congress can propose an amendment to the Constitution

Congress can propose amendments to the states by a two-thirds vote in each house. Neither party has come close to that threshold in recent decades.

A successful constitutional amendment must appeal to many members of both parties. If all members of the majority party support an amendment, roughly 70 members of the minority party in the House and 14 in the Senate must agree. Most likely, and ideally, minority-party support would be substantially greater.

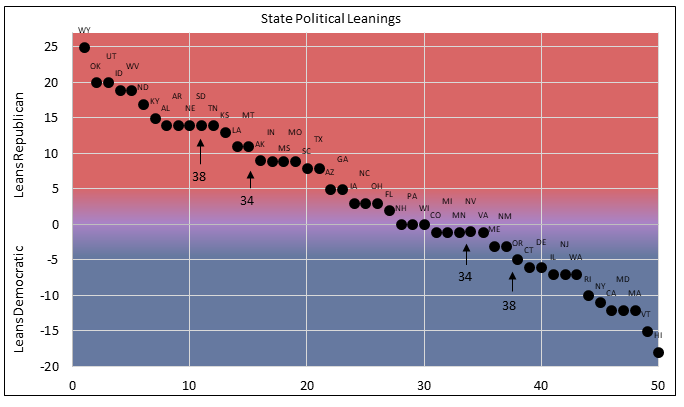

Figure 8. Three-fourths of state legislatures can ratify proposed amendments

Source: Cook Political Report

After Congress proposes an amendment to the Constitution, state legislatures can consider it. Once three-fourths of state legislatures have approved an amendment, it is ratified and becomes part of the Constitution.

A three-fourths threshold requires thirty-eight of the fifty state legislatures. This ensures broad consensus across ideological, regional, and other lines. It also minimizes the chance that an ill-formed or ill-considered amendment could be adopted.

The other, less-traveled path of ratification in the Constitution is by conventions in each state. Conventions ratified the Constitution, but Congress only chose this route for the 21st Amendment to repeal alcohol prohibition. Nonetheless, the convention mode also would require a proposed amendment to have broad appeal.

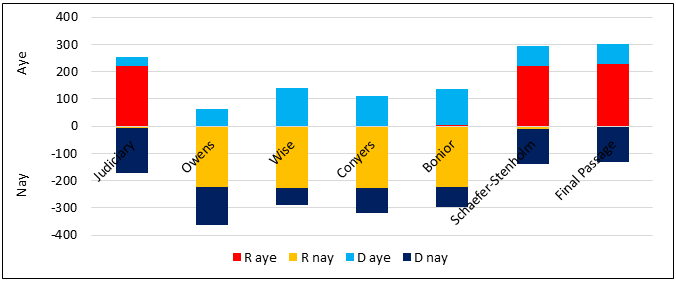

Figure 9. The 1995 House Queen-of-the-Hill rule embraced competition

Source: Congressional Record

The House approved a BBA in 1995 by a 300-132 vote. After robust markups in the House and Senate Judiciary Committees, the House adopted a rule for a “queen of the hill” process10: the substitute amendment with the most votes would become the text for the vote on final passage. Members could vote for any BBA they supported.

The House considered six substitute amendments: a conservative BBA reported from the Judiciary Committee, four Democrat-proposed BBAs, and one with broad, bipartisan support.11 A coalition of 72 Democrats and all-but-two Republicans approved the bipartisan Stenholm-Schaefer BBA on final passage.

The Senate took up the House-passed BBA with extensive floor debate and amendment consideration. The vote on final passage was one vote short of the 67 needed.

These votes followed decades of bipartisan cooperation on BBA proposals. Congress and Presidents Reagan, Bush, and Clinton had pursued deficit reduction for over a decade, and as Figure 2 shows, the federal government was under fiscal pressure then.

That nearly-successful BBA had shortcomings, however, about which many members raised concerns. Today, next-generation BBAs may have greater appeal.12

Figure 10. Medium-term “structural” balance supports stable & predictable policy

Source: CBO, author’s calculations

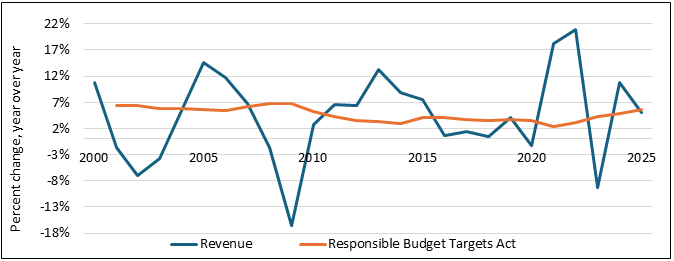

Annual balance is the key defect in most BBAs. Revenue varies a lot from year to year (blue line). Tying spending – especially “outlays” instead of “expenditures” – to revenue each year would exhaust policymakers with shifts in spending and revenue policies. The additional uncertainty would reduce investment, prosperity, and opportunity.

The alternative is balance over the medium term, also known as structural balance or balance over the business cycle. Structural balance can temper revenue fluctuations and provide a stable, predictable, and practical set of budget targets to guide Congress’ budget decisions. Several other countries and U.S. states have already adopted this income-smoothing.

Rep. Jodey Arrington’s Business Cycle BBA would do this by limiting spending to a rolling average of inflation-and-population-adjusted revenue from the prior three years. Rep. Nathaniel Moran’s Principles-based BBA would empower Congress to enact statutes with details and mechanisms. This could include Rep. Tom Emmer’s and then-Sen. Mike Braun’s Responsible Budget Targets Act (orange line),13 which resembles the statutory side of the Swiss debt brake. Either BBA would let Congress choose between full balance and primary balance, which excludes interest costs and would be similar to the European Union’s 3 percent deficit limit.

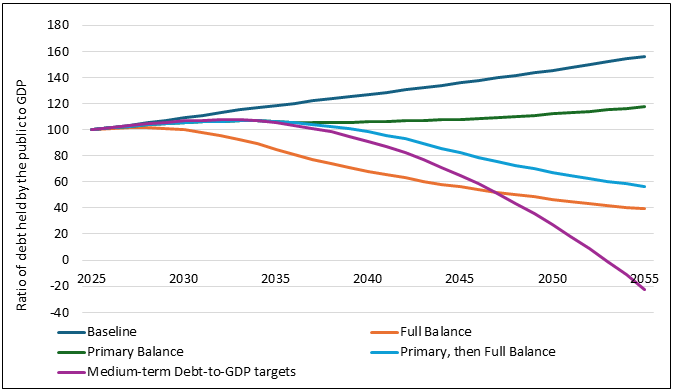

Figure 11. Primary balance is a reasonable initial target

Source: CBO LTBO, author’s calculations

Reducing the debt burden – the debt-to-GDP ratio – is a key metric for evaluating fiscal space and health. Some have proposed budget targets based directly on the debt-to-GDP ratio. That approach is intellectually sound, although it may not be as intuitive for the public as some form of balanced budgets.

Fortunately, however, a ten-year transition to primary balance, which excludes interest expenses, provides a similar glide path to at least one variation on debt-to-GDP targets over a decade or so: each year, requiring Congress to reduce the projected debt-to-GDP ratio at the end of five years by one percentage point compared to the baseline.

Similarly, a ten-year path to full balance is theoretically possible but would require more than twice the fiscal consolidation of a transition to primary balance.14 Comparing the gaps between the baseline and the balance targets shows this clearly. Primary balance may not be enough to control the long-term debt burden, but after reaching primary balance, Congress could move toward full balance with targets for primary surpluses.

Figure 12. Federal capital spending is relatively small, but BBAs would treat differently

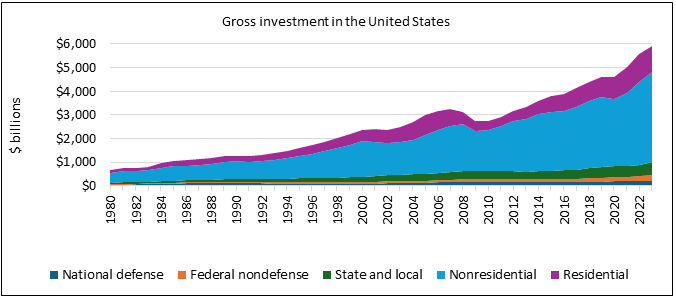

Source: Bureau of Economic Analysis

Federal spending provides a small share of gross investment in the United States: less than state and local government investment and much less than private investment.

Some believe a BBA should exclude capital expenditures. After all, state balanced budget requirements generally apply to operating budgets. On the other hand, capital projects provide value over an asset’s useful life and thus balance in a sense over a longer horizon. Still, smoothing the costs of investment over time may be more relevant at local levels of government where capital spending is lumpy.

That said, a well-crafted BBA could let Congress practice capital budgeting even without explicit mention in the amendment. Many BBAs’ limits on “outlays” would not permit that, however, which would also create management challenges for the executive branch on the timing of expending funds.

Using “expenditures” instead could let Congress add budget authority to capital funds, and the executive branch could outlay the funds as grants and contracts are ready to pay out. A principles-based BBA could, in addition, let Congress design implementing legislation to balance the normal budget over the medium term, offset emergencies subsequently over multiple years, and smooth the costs of capital expenditures over assets’ useful lives.

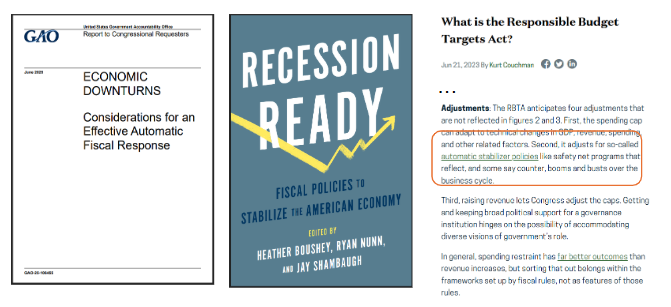

Figure 13. Implementing legislation can accommodate automatic stabilizers

Sources: GAO, Brookings, Americans for Prosperity15

“Automatic stabilizers” are increases in spending and reductions in revenue that occur without new congressional action and reduce business cycle fluctuations according to Keynesian and related economic theories. For example, during a recession, reductions in incomes and employment increase demand for unemployment, nutrition, and health programs.

The Government Accountability Office has recommended options to improve these automatic responses. Experts with the Brookings Institution’s Hamilton Project published Recession Ready, a book advocating for more robust automatic stabilizers.

Whatever the features of those programs may be, implementing legislation for a well-written balanced budget amendment can accommodate Congress’ preferences. For example, the Responsible Budget Targets Act would adjust its revenue-based spending targets for automatic stabilizers, changes in revenue, emergency spending, and other factors.

Figure 14. Two-thirds is the legislative supermajority for exceptional situations

| Threshold | Purpose* |

| One-fifth | Recorded vote |

| Majority | Choose officers, impeach (House), quorum, make rules, punish members, initially approve legislation, approve other actions, break Electoral College ties, approve nominations (Senate), approve nominee for vice president vacancy, VP and majority of other officers notify Congress that POTUS cannot discharge duties |

| Three-fifths | Counting enslaved persons for House apportionment (defunct) |

| Two-thirds | Try impeachments (Senate), expel members, veto overrides, approve treaties (Senate), propose amendments to Constitution, apply for amendment convention (state legislatures), quorum for breaking Electoral College ties, remove barriers to certain participants in insurrections or rebellions from holding public office, affirm that POTUS is unable to discharge the powers and duties of his office |

| Nine-thirteenths | Original ratification of Constitution by state conventions |

| Three-fourths | State legislatures or conventions ratify proposed amendments to Constitution |

*Applies to each house of Congress unless otherwise specified.

Source: U.S. Constitution

Congress needs the independent ability to borrow. The challenge is to balance Congress’ ability to respond quickly to serious emergencies with a high-enough threshold to discourage abuse.

BBA proposals contain diverse thresholds for setting aside the balance rule and other provisions. Three-fifths is commonly proposed, but that threshold has no current application in the Constitution. Three-fourths appears too, but the Constitution only uses that fraction for the ratification phase of constitutional amendment proposals, and it exceeds the threshold for overriding the president’s veto. Simple majorities clearly do not limit excessive borrowing.

BBAs with different thresholds for different scenarios may create perverse incentives. For instance, majorities to waive balance for military conflicts but supermajorities for other reasons could encourage hostilities for fiscal purposes.

Two-thirds is the most common constitutional threshold for unusual circumstances, including for overriding a president’s veto.

Some BBAs propose tying a threshold to the “whole number” of members or similar concepts. This, too, is alien to constitutional provisions relating to legislation, and a simple majority of the whole number for revenue increases could inadvertently override the Senate’s filibuster for revenue measures.

Figure 15. Most emergency votes greatly exceed two-thirds

| Legislation | Year | House* | Senate |

| Declaration of War: World War I | 1917 | 88.2% | 93.2% |

| Pre-WWII Appropriations | 1940 | 99.7% | 100.0% |

| WWII Declaration of War: Germany | 1941 | 100.0% | 100.0% |

| WWII Declaration of War: Italy | 1941 | 100.0% | 100.0% |

| WWII Declaration of War: Japan | 1941 | 99.7% | 100.0% |

| Cuban Missile Crisis Resolution Authorizing Force | 1962 | 98.2% | 98.9% |

| Gulf of Tonkin Resolution | 1965 | 100.0% | 97.8% |

| Operation Desert Shield Appropriations | 1990 | 90.3% | Unanimous Consent |

| Authorization for Use of Military Force against Iraq | 1991 | 57.7% | Unanimous Consent |

| Y2K Preparation | 1999 | 94.4% | 81.8% |

| Defense and Emergency Appropriations, FY 2002 | 2001 | 98.6% | 97.9% |

| 9/11 Response Supplemental Appropriations | 2001 | 100.0% | Unanimous Consent |

| 9/11 Authorization of Military Force | 2001 | Unanimous Consent | 100.0% |

| Supplemental Appropriations, FY 2002 | 2002 | 92.5% | 92.9% |

| Authorization for Use of Military Force in Iraq | 2002 | 69.0% | 77.0% |

| Hurricane Katrina Response | 2005 | Voice Vote | Unanimous Consent |

| Hurricane Katrina Supplemental Appropriations | 2005 | 97.4% | 100.0% |

| Bush 2008 Stimulus Bill | 2008 | 91.8% | 83.5% |

| Emergency Economic Stabilization Act of 2008 (TARP) | 2008 | 60.6% | 74.7% |

| Supplemental Appropriations Act, 2009 | 2009 | 52.8% | 94.8% |

| American Recovery and Reinvestment Act of 2009 | 2009 | 57.3% | 61.2% |

| Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020 | 2020 | 99.5% | 99% |

| Families First Coronavirus Response Act of 2020 | 2020 | 90.1% | 91.8% |

| CARES Act of 2020 | 2020 | Voice Vote | 100% |

| Consolidated Appropriations Act, 2021 | 2020 | 79.4% | 93.9% |

| American Rescue Plan Act | 2021 | 50.8% | 50.5% |

Source: Library of Congress

Congressional votes for emergencies usually exceed two-thirds.

Lower support usually reflects the inclusion of provisions beyond those directly related to the emergency at hand. A higher threshold would discourage extraneous provisions.

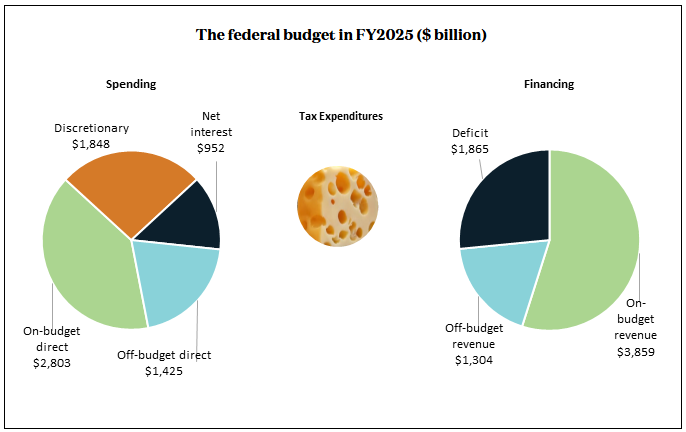

Figure 16. A comprehensive budget would let Congress achieve balance and more

Source: CBO

The annual appropriations process (orange) excludes three-fourths of federal spending, all revenue, and the foregone revenue from tax expenditures. Budget reconciliation is irregular and partisan, limiting bipartisan efforts to improve efficiencies in direct spending programs. Social Security, new borrowing, and interest expenses are entirely absent from either.

A real budget would be a single bill for Congress to review and manage all spending, revenue, tax expenditures, and borrowing. Giving all members and committees larger stakes in the annual budget process could improve Congress and deliver better results for the American people.

The Comprehensive Congressional Budget Act16 by Rep. Blake Moore would build on the Congressional Budget Act of 1974: the Appropriations Committees would keep managing discretionary spending, and all other committees could manage their direct spending and revenue portfolios. The result would be an annual budget act built mostly in the committees, and it would offer many more opportunities for collaboration and coalition building.

Expanding buy-in and the potential scope of revisions would give Congress the means and the motivation to reach and sustain reasonable budget targets.

Figure 17. Many amendment proposals include barriers to broad appeal

Diverse BBAs and other fiscal responsibility amendments (FRAs) contribute to the conversation about rules-based responsible budgeting.

Even so, many include provisions that are barriers to adoption. Proposals are often long, complicated, and detailed. They would frequently target annual balance, aim for full balance, or provide little time to reach balance. Some refer to statutory items like “outlays,” the debt limit, or even specific programs. Some provisions have broad opposition or could alter the balance of powers, such as putting the president’s budget request in the Constitution. Multiple emergency thresholds are common, which could encourage military conflict.

The color-coding is not a value judgment on the provisions per se. Instead, it signifies obstacles to broad support within Congress and state legislatures based on legislative history.

- Red: Fatal. E.g., excluding major programs; supermajorities to raise revenue.

- Orange: Major headwinds. E.g., annual balance; statutory debt limit.

- Yellow: Not ideal but tolerable to many. E.g., full balance; several emergency exceptions.

- Green: Broadly acceptable. E.g., allow medium-term and primary balance.

Conclusion: A well-written BBA can help Congress restore fiscal democracy

The U.S. federal government’s financial condition is increasingly perilous. The federal debt burden and interest expenses are reaching unprecedented levels that drive higher inflation and interest costs for governments and households. They undermine prosperity and opportunity while contributing to polarized politics.

Members of Congress largely know what must be done. They do not know, however, how to do it and survive politically. Improvements to budget practices can help.

A well-crafted balanced budget amendment to the Constitution, implementing legislation, and upgrades to the annual budget cycle can give members appropriate kinds of political cover while facilitating bipartisan deal-making to produce more efficiency and greater value for the American people every year.

U.S. states and other countries have relied on combinations of policy changes and institutional improvements to reverse fiscal stress and improve governance. Next-generation BBA proposals resolve the obstacles to success that have hindered earlier attempts, and they would provide stable and predictable foundations for deliberative policymaking within Congress.

The U.S. can avoid stagflation, debt crisis, and indiscriminate cuts if Congress acts to strengthen itself soon. Better ways of doing business can make congressional service far more fulfilling while also defusing the debt threat and addressing other challenges.

For the full document, click here.