The House Judiciary Committee had planned – now delayed – to mark up a balanced budget amendment (BBA) following a hearing last month. Most BBAs would require spending and revenue to balance. Ideally, that would happen over the medium term, not each year.

In the states, however, borrowing restraints are often debt limits. Representative Tom McClintock’s H.J.Res.9 proposes the same:

Section 1. The United States Government may not increase its debt except for a specific purpose by law adopted by three-fourths of the membership of each House of Congress.

Section 2. This article shall take effect beginning ten years after its ratification.

In 38 words, these principles resemble existing constitutional language. They leave many questions for Congress to answer with statutes that can adjust with America’s changing needs.

The right definition makes all the difference

Defining “increase its debt” or even just “debt” is key.

It could reflect the statutory debt limit, which applies to the nominal gross federal debt, or nominal debt held by the public, which excludes trust fund assets.

This would carry the political baggage of the statutory debt limit, magnified by constitutional heft. If this were the only way, the amendment would face stiff headwinds toward two-thirds support in both houses and from three-fourths of state legislatures. But another way is possible.

Congress could define “debt” as the ratio of debt held by the public to gross domestic product (debt-to-GDP). This ratio is growing too but more slowly than the nominal debt.

Debt-to-GDP targets could also adjust over the business cycle for so-called automatic stabilizers: benefit programs expand when more people are out of work and down, and revenue collections are lower.

Alternatively, or in addition, the government could build cash balances when the economy is strong and draw on them when times are tough. States do this regularly to smooth budgeting over the business cycle.

A transition to stabilizing the debt

The amendment would give Congress ten years after ratification to stabilize the debt. This would be challenging, even with a multi-year ratification period.

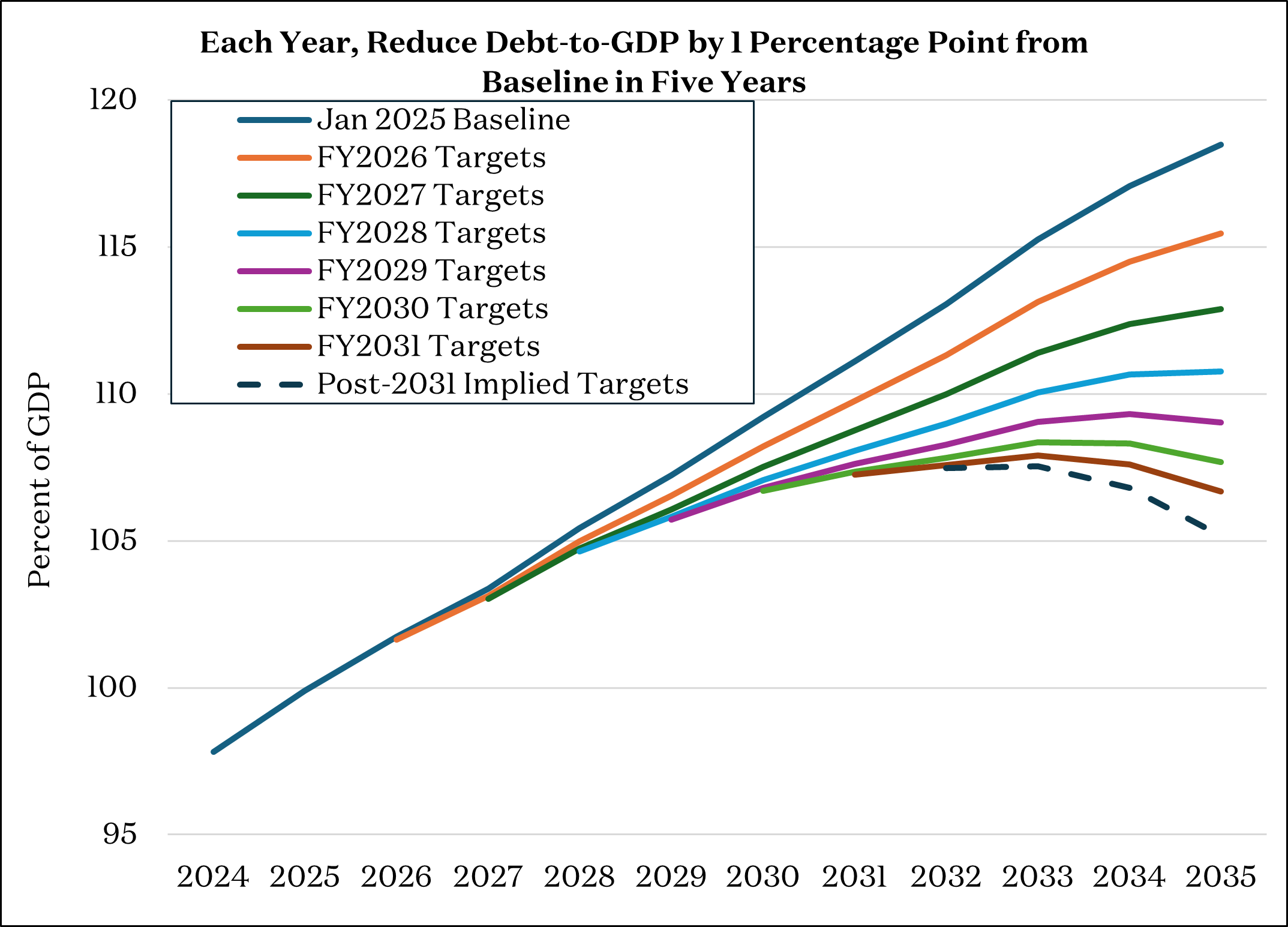

Figure 1 illustrates repeatedly meeting modest medium-term debt-to-GDP targets. Each year, Congress would reduce the debt-to-GDP ratio after five years to one percentage point lower than the latest projection. Any combination of spending restraint, revenue, and economic growth could contribute. The debt would stabilize and start to decline within a decade.

Figure 1: Medium-term debt-to-GDP targets can turn the debt track

A stable-but-high debt burden still has costs. Debt beyond about 70 percent of GDP drags on economic growth by diverting investment funds from productive uses to merely covering past government borrowing. Reducing the debt further would make space for emergency borrowing while avoiding debt drag.

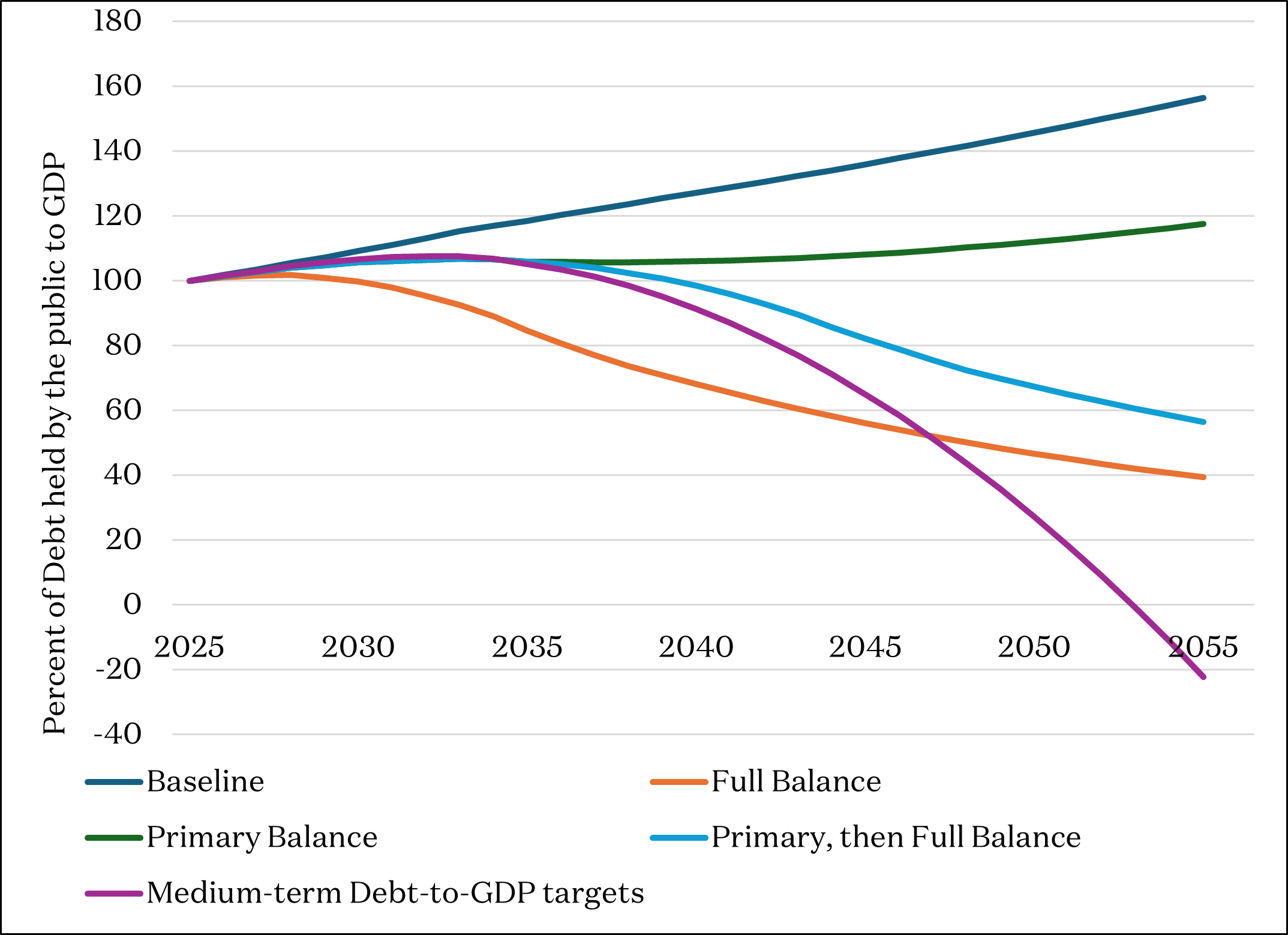

Figure 2 looks out 30 years alongside other scenarios. Continuing to reduce the debt burden as above could fully eliminate the debt.

Figure 2: Statutory debt-to-GDP targets should adjust as conditions change

But Congress need not pay off the debt entirely. Some is worth keeping: low-risk government debt supports robust and flexible markets that deliver opportunity and prosperity.

Instead, just as a driver lightens up on the gas when reaching cruising speed, debt-to-GDP targets could moderate at key thresholds:

- when the debt-to-GDP ratio starts to decline,

- when the debt burden falls below 70 percent, and

- when it reaches, say, 40 percent of GDP.

Congress could update these statutes as times change.

Enforcement

More sophisticated automatic enforcement could help Congress meet its targets. Rather than sequestration’s goofy meat axe, a surgical approach could instruct OMB to use lists of spending and revenue tweaks to reach savings objectives.

Even better, a comprehensive congressional budget with all spending and revenue would maximize the regular order options available to Congress to reach budget goals. Authorizing committees would join the Appropriations Committees in managing their fiscal portfolios within limits each year. All members could contribute much more to federal budgeting in a bottom-up, collaborative, committee-driven process.

Conclusion

Mr. McClintock’s debt limit amendment would empower Congress to develop and adjust the details by statute. Medium-term debt-to-GDP targets could be a solid foundation for thoughtful, practical budgeting, especially with complementary upgrades.

Kurt Couchman is a Senior Fiscal Policy Fellow at Americans for Prosperity.