Chairman Arrington, Ranking Member Boyle, and members of the committee:

Thank you for continuing to consider systemic solutions to the federal government’s systemic problems. I am pleased to share thoughts on proposals for a neutral, practical balanced budget amendment (BBA) to the Constitution and related statutory upgrades that should also appeal to supermajorities of members. Controlling the debt burden can protect Americans from higher costs, expand opportunity, and defuse the threats to prosperity, security, and even our political system from a debt crisis.

The Budget Committee’s role in coordinating federal spending, revenue, deficits, and debt provides crucial insights for fiscal responsibility amendment proposals. Most implementing legislation would be within the Budget Committee’s responsibility for “budget process generally” and “establishment, extension, and enforcement of special controls over the Federal budget.”[1] Perhaps building out clear solutions with wide appeal would increase confidence that a well-written BBA would be a solid foundation for more effective, responsible, and rewarding federal budgeting.

These remarks begin by outlining the overwhelming support for the concept of balancing the federal budget. They then move to design considerations for restoring the balance norm through an amendment to the United States Constitution. It concludes noting how a BBA can encourage Congress to upgrade federal budget statutes with best practices.

Thomas Jefferson wished for a constitutional amendment “taking from the federal government the power of borrowing.”[2] James Madison called government debt a “public curse.”[3] For 150 years, the federal government borrowed only in exceptional times and otherwise reduced the debt burden.

That changed in the Great Depression. Then, a Maryland Democrat proposed a resolution calling for the return of balanced budgets in 1935, and a Minnesota Republican introduced the first true BBA the following year.[4] Congressional proposals and state applications for an amendment convention have often had bipartisan support, although this softened when House Republican leaders made a BBA a political priority in 1994. Even then, opponents of the nearly successful BBA in early 1995 asserted “We agree with the Committee majority that the Federal Government should maintain a balanced budget… Congress must take dramatic action to reduce the deficit and place the Nation on a course of sound fiscal management.”[5]

Following the 2011 debt limit deal, twenty-five House Democrats joined nearly all Republicans in supporting a BBA on the House floor,[6] and another sixteen Democrats supported other versions.[7] In the Senate, twenty Democrats and one Republican voted for one version while all Republicans supported another.[8] Each BBA proposal had substantial design flaws.

In the states, each except Vermont has constitutional or statutory requirements for balanced operating budgets.[9] They take different forms, apply at different stages, and vary in stringency. Most states adopted fiscal controls after experiencing budget problems or witnessing other states’ mishaps.[10]

Looking abroad, many national governments have a balanced budget requirement, often supplemented by a debt or spending limit. Of thirty-five advanced economies, only Greece, Spain, Canada, and the United States have no national-level balance rule.[11]

Back home, a July 2023 poll found that 80 percent of Americans support “a constitutional amendment that would require a balanced budget within 10 years.” Support by party affiliation was 83 percent of Republicans, 79 percent of Democrats, and 76 percent of independents.

That said, in a 2000 poll of economists, 87.7 percent agreed with the statement, “If the federal budget is to be balanced, it should be done over the course of the business cycle rather than yearly.”[12]

Finally, a balanced budget amendment is best thought of as the flagship of a flotilla of fiscal fixes. A politically plausible BBA can’t address everything. It can, however, strengthen the balance norm and provide momentum for Congress to build out better budget practices.

The growing debt burden, ongoing inflation and interest rate pressures, and increasing federal interest costs[13] may restore the bipartisan consensus for deficit reduction that existed in the 1980s and 1990s. Yet the Clinton-Gingrich surpluses reflected both hard work and luck.

Rather than those fortunate tailwinds, Congress now faces headwinds and will need substantial institutional upgrades to get back on track. The good news is that the same solutions to our fiscal challenges can help members of Congress be more effective legislators while making America’s legislature a far more rewarding place to serve.

Translating support for the principles of balance into the concrete language of a constitutional amendment is challenging. Most BBA proposals have significant shortcomings, but not all.[14]

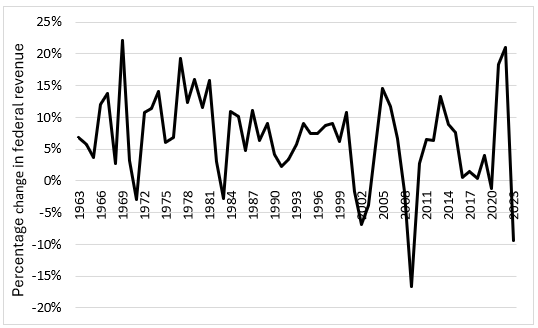

The Balance Rule: Annual balance is the fatal flaw of most BBA proposals, including every version that has come to a vote in Congress. Revenue is volatile from year to year. Tightly binding spending to revenue with balance every year would cause tremendous policy instability, as Figure 1 indicates.

Source: CBO

A reasonable desire to avoid regular, substantial changes to spending and revenue policies would encourage Congress to evade annual balance requirements. Disregarding a constitutional provision, however, may undermine public perceptions of Congress’ commitment to the rule of law.

Several strategies to avoid the straitjacket of annual balance exist. After all, fiscal responsibility reflects medium- and long-term trends of revenue and spending, not the outcomes of any given year.

Chairman Arrington’s “Business Cycle Balanced Budget Amendment” prescribes a specified relationship between spending and revenue: “Total expenditures for a year shall not exceed the average annual revenue collected in the three prior years, adjusted in proportion to changes in population and inflation.”[15] This creates a smooth, predictable path for non-emergency fiscal policies with narrower scope for estimates.

Another option is proposing general principles and relying on implementing legislation for the details.

Representative Moran and Senator Braun’s “Principles-based BBA” takes this approach: “Expenditures and receipts shall be balanced, which may occur over more than one year.”[16] The heart of implementing legislation for such a BBA might resemble Senator Braun and Representative Tom Emmer’s Responsible Budget Targets Act. This bill would set up a glide slope to structural primary balance, which would balance revenue and non-interest spending over the medium term, while adjusting for revenue policy changes and automatic stabilizers and offsetting emergency spending in subsequent years.[17] The adjustment for automatic stabilizers would let the budget be countercyclical, to use the language of Keynesian macroeconomics.

Representative McClintock’s proposal for a constitutional debt limit also sets out a principle: “The United States Government may not increase its debt except for a specific purpose by law adopted by three-fourths of the membership of each House of Congress.”[18] Thoughtful definitions and creative uses of cash balances and reserve funds could make such a debt limit more practical than it may initially appear.

Broad principles may be attractive for constitutional provisions. Most existing provisions are more like principles, and they let Congress adjust statutory details as national needs change.

In addition, Chairman Arrington and Representative Moran’s proposals exclude “payment of debt” from the expenditures that must balance with revenue. Other BBAs exclude “repayment of debt principal.” This distinction matters.

“Payment of debt” lets Congress decide whether to target full balance or primary balance, which excludes interest expense, while most are limited to full balance. Reaching full balance over the next decade would require about $15 trillion in deficit reduction over a decade, including avoided interest costs. A path to primary balance would mean about $6 trillion in primary deficit reduction over ten years and would approximate the European Union’s requirement for members’ overall deficits to stay below three percent of GDP.[19]

Finally, the Arrington and Moran proposals use the term “expenditures” for spending instead of “outlays.” “Expenditures” is a general term that already exists in the Constitution and can cover the range of statutory definitions for spending, especially “budget authority.”

“Outlays” is, however, defined in statute and applies when funds transfer to a non-federal entity. Simplifying, Congress controls budget authority directly, while the executive branch converts budget authority into outlays. A constitutional limit on outlays would create unnecessary management challenges. Limiting outlays would also increase the difficulty of establishing a capital budget, although CBO’s first director, Democratic appointee, and Brookings Institution scholar Alice Rivlin recommended against Congress doing so before this committee in 2012.[20]

Safety valve: Congress must be able to spend extra for war, recession, pandemics, natural disasters, and otherwise. A BBA’s safety valve must be high enough to limit abuse yet low enough for Congress to address the unexpected. Preserving fiscal space for emergency response is a key reason to control the debt otherwise.

The Arrington and Moran BBAs would authorize Congress to make emergency expenditures with a two-thirds vote in each house. This universal threshold equals the veto override and is the highest level applicable to congressional approvals.

The McClintock debt limit would require three-fourths support in both houses for emergency borrowing. This threshold appears in the Constitution for ratifying proposed constitutional amendments in the states. Congress has, however, typically approved emergency spending with margins well above this level.

Three-fifths is often the all-purpose threshold for setting aside BBA requirements, but this level is the same as the Senate’s filibuster and seems to have provided only modest restraint against overuse of emergency designations. It appears nowhere in the Constitution with respect to congressional procedures.

Some BBA proposals have several emergency thresholds.[21] For instance, some would automatically suspend requirements during a declared war or by mere majorities in case of overseas military contingencies. Most do not limit extra spending to the security threat, which would create a perverse incentive to support kinetic military action to avoid fiscal responsibility. Matters of war and peace should be considered on their own merits.

Transition to balance: The pace of the glide path must weigh many factors.

The ratification period would give Congress a modest buffer between proposing a BBA to the states and its incorporation into the supreme law of the land. Two to three years to ratify is a reasonable guess based on prior amendment consideration by often-part-time state legislatures.

The Arrington, Moran, and McClintock proposals would give Congress ten years after ratification to reach balance, however defined, as would BBAs from Reps. Perry, Van Orden, Loudermilk, and Mace.[22] Chairman Arrington’s BBA specifies the transition through the ingenious use of declining fractions. Other proposals would leave Congress the discretion to choose the path in implementing legislation or otherwise.

BBA proposals from Reps. Buchanan, Fitzpatrick, Nunn, Obernolte, Yakym, and Gluesenkamp Perez would provide five years.[23] Rep. Biggs’s proposal would require balance immediately upon ratification, while Rep. Pfluger’s would allow two years after ratification.[24]

Statutory items: Constitutional language is generally written in normal English. No existing provision refers to a statutory term or program, although that’s mostly because statutes came after and flowed from authorities in the Constitution.

Even so, amending the Constitution is extraordinarily difficult and much more so than changing statute. Embedding statutory constructs in the Constitution risks propping up outdated approaches as well as letting anachronisms accumulate if Congress changes applicable laws.

The previous discussion of “outlays” compared to “expenditures” is one such example.

Another is the statutory debt limit. Admittedly, debt limit deals have been important moments for Congress to adopt deficit-reducing packages and budget process upgrades.[25] That has waned in recent years, but perhaps it can build next year where last year’s Fiscal Responsibility Act left off.

The statutory debt limit is derived from and partly delegates Congress’ Art. 1, Sec. 8, cl. 2 power “To borrow Money on the credit of the United States.” After ratifying, implementing, and living with a BBA and related budgetary changes, Congress may find that the statutory debt limit is a vestigial organ it can do without. Then again, automatically suspending the debt limit only as long as the budget stays on target could be part of budget enforcement.

The president’s annual budget request is another.[26] The president’s current budget powers are largely signing or vetoing bills and otherwise taking care that the laws are faithfully executed. Putting the president’s budget proposal in the Constitution is unnecessary and risks changing the balance of powers.

Political barriers: Some BBA proposals have provisions that many members of Congress cannot accept. They are significant barriers to achieving two-thirds support in both houses, and some raise policy concerns as well.

Some propose supermajorities to increase revenue. Reducing low-value spending, including spending through the tax code, could provide most or perhaps all savings needed to balance the budget. Yet decisions about policy changes belong within the normal give and take of congressional deliberation. A BBA provision meant to put a thumb on the scale for substantive preferences that are not broadly shared reduces the chances that a BBA can be adopted.

Similarly, some BBAs would require supermajority votes to exceed a prescribed spending-to-GDP ratio. Those of a more limited government perspective might worry that this ceiling would become a floor and become an obstacle to their preferred size and scope of the federal government’s activities. Conversely, those who believe the federal government should be able to do more than the proposed spending cap would obviously object. Moreover, from a good government perspective, such a limit could be evaded to some degree by converting spending into mandates and tax preferences.

Some BBA proposals would exclude Social Security and Medicare spending and revenue from the balance calculation. Aside from referencing statutory programs, this would remove the programs that drive the long-term deficits[27] from the amendment allegedly meant to help Congress restore a sustainable fiscal outlook. Merely including all spending and revenue in a fiscal rule does not imply that Congress would treat all programs equally or that Congress would design automatic enforcement to apply equally, at least as long as Congress can move beyond the ineffective sequester paradigm.

Open questions: Some BBAs propose to constrain court-ordered policy changes, such as those by Reps. Loudermilk and Pfluger and Senator Lee.[28] The Constitution gives Congress some ability to shape courts’ jurisdiction, but that may not be sufficient to prevent court encroachment on Congress’ legislative powers over spending and revenue policymaking.

On the one hand, courts play an important role in our system of checks and balances, and they can add weight to enforcement procedures and call out constitutional improprieties by the other branches. On the other hand, spending and revenue decisions are inherently legislative functions that require accommodating diverse views and interests. This is a different mental model from the judicial roles of deciding questions of laws and fact.

The degree to which latent court authority matters may depend on the credibility of statutory solutions for implementing a BBA along with the public’s expectation that Congress will follow a new constitutional provision. A Congress with the means and motivation to manage the entire budget[29] to meet balance and other goals may be able to stave off judicial intervention even if the door remains open.

Even so, whether and in what form constitutional or statutory language constraining or empowering the courts in the context of a balanced budget amendment will be an important question for Congress to consider.

Law professor Rob Natelson has argued that Congress tends to respect constitutional provisions, if imperfectly, because the public expects them to.[30] A well-crafted balanced budget amendment is probably necessary to restore the norm that the federal government should live within its means outside of emergencies. It is unlikely to be sufficient, however.

Managing the entire federal budget to meet balance goals would be a complicated endeavor. Implementing legislation that defines terms, specifies mechanics, and sets out politically sustainable enforcement tools[31] would be crucial. A BBA-related, national conversation on returning to fiscal responsibility would encourage Congress to revise and upgrade the details of the process.

An annual budget process that starts on time, ends on time, and gives all members opportunities to make productive contributions[32] could provide the stable, predictable, neutral platform on which members of Congress can build coalitions on a wide variety of policy agreements. Reaching and sustaining balanced budgets is among many possible benefits.

An effective budget process could also improve the collaborative culture of Congress, unleash the entrepreneurial and innovative spirit of members to improve the federal government’s value for the people, and help members make regular, incremental progress toward resolving a wide variety of challenges while modernizing policies to match today’s and tomorrow’s needs.

A proposed or ratified balanced budget amendment would focus Congress on overhauling a system that is failing to serve our country well. Without such motivation, Congress may not act soon enough to prevent escalating pain and suffering as interest rates rise and the debt burden grows with ever-greater risk of stagnation and fiscal crisis.

Fortunately, restoring the balance norm has strong support, and new versions resolve the design problems of earlier versions. With a BBA and related statutory changes, bottom-up, bipartisan deal-making within an effective budget process can make America’s future brighter than ever.

[1] https://rules.house.gov/sites/evo-subsites/republicans-rules.house.gov/files/documents/118/Additional%20Items/118-House-Rules-Clerk-v2.pdf, Rule X(1)(d)

[2] https://tjrs.monticello.org/letter/178

[3] https://founders.archives.gov/documents/Madison/01-13-02-0106

[4] https://crsreports.congress.gov/product/pdf/R/R41907

[5] https://www.congress.gov/104/crpt/srpt5/CRPT-104srpt5.pdf, “Minority views of Messrs. Kennedy, Leahy, and Feingold”

[6] https://clerk.house.gov/Votes/2011858

[7] https://www.congress.gov/bill/112th-congress/house-joint-resolution/10, https://www.congress.gov/bill/112th-congress/house-joint-resolution/81, https://www.congress.gov/bill/112th-congress/house-joint-resolution/87, https://www.congress.gov/bill/112th-congress/house-joint-resolution/89

[8] https://www.senate.gov/legislative/LIS/roll_call_votes/vote1121/vote_112_1_00228.htm https://www.senate.gov/legislative/LIS/roll_call_votes/vote1121/vote_112_1_00229.htm

[9] https://www.nasbo.org/reports-data/budget-processes-in-the-states

[10] https://americansforprosperity.org/wp-content/uploads/2022/11/AFP-States-can-unleash-freedom-and-reclaim-sovereignty-with-structural-balance.pdf, https://www.mercatus.org/research/working-papers/outlawing-favoritism-economics-history-and-law-anti-aid-provisions-state

[11] https://www.imf.org/external/datamapper/fiscalrules/matrix/matrix.htm

[12] https://cclark.gcsu.edu/Survey%20of%20Republicans,%20Democrats,%20and%20Economists.pdf

[13] https://www.fiscal.treasury.gov/files/reports-statements/mts/mts0924.pdf, Table 3

[14] https://americansforprosperity.org/press-release/a-better-balanced-budget-amendment-can-succeed/

[15] https://www.congress.gov/bill/118th-congress/house-joint-resolution/113

[16] https://www.congress.gov/bill/118th-congress/house-joint-resolution/80

[17] https://americansforprosperity.org/blog/responsible-budget-targets-act/

[18] https://www.congress.gov/bill/118th-congress/house-joint-resolution/9

[19] https://www.consilium.europa.eu/en/policies/excessive-deficit-procedure/

[20] https://www.congress.gov/event/112th-congress/house-event/LC3155/text

[21] https://www.congress.gov/bill/118th-congress/house-joint-resolution/12

[22] https://www.congress.gov/bill/118th-congress/house-joint-resolution/19, https://www.congress.gov/bill/118th-congress/house-joint-resolution/21, https://www.congress.gov/bill/118th-congress/house-joint-resolution/75, https://www.congress.gov/bill/118th-congress/house-joint-resolution/90

[23] https://www.congress.gov/bill/118th-congress/house-joint-resolution/2/, https://www.congress.gov/bill/118th-congress/house-joint-resolution/6, https://www.congress.gov/bill/118th-congress/house-joint-resolution/12, https://www.congress.gov/bill/118th-congress/house-joint-resolution/15,

https://www.congress.gov/bill/118th-congress/house-bill/9353

[24] https://www.congress.gov/bill/118th-congress/house-joint-resolution/36, https://www.congress.gov/bill/118th-congress/house-joint-resolution/55, https://www.congress.gov/bill/118th-congress/house-joint-resolution/67

[25] https://www.crfb.org/papers/qa-everything-you-should-know-about-debt-ceiling#appendix

[26] https://uscode.house.gov/view.xhtml?req=granuleid:USC-prelim-title31-section1105&num=0&edition=prelim

[27] https://bipartisanpolicy.org/download/?file=/wp-content/uploads/2024/08/BPC_Grand_Market_Committee_Paper-3.pdf, see Fig. 6

[28] https://www.congress.gov/bill/118th-congress/house-joint-resolution/67, https://www.congress.gov/bill/118th-congress/house-joint-resolution/75, https://www.congress.gov/bill/118th-congress/senate-joint-resolution/14

[29] https://americansforprosperity.org/blog/what-is-the-comprehensive-congressional-budget-act/

[30] https://www.theepochtimes.com/understanding-the-constitution-constitutional-amendments-work_4027117.html

[31] https://americansforprosperity.org/blog/automatic-budget-enforcement/

[32] https://americansforprosperity.org/blog/what-is-the-submit-it-act/, https://www.crfb.org/papers/better-budget-process-initiative-automatic-crs-can-improve-appropriations-process, https://americansforprosperity.org/blog/what-is-the-comprehensive-congressional-budget-act/

© 2026 AMERICANS FOR PROSPERITY. ALL RIGHTS RESERVED. | PRIVACY POLICY

Receive email alerts to learn how to get involved